The Power of a Personal Balance Sheet

When starting a journey, it's helpful to know where you are starting from.

Having a firm grasp on your assets and liabilities—and, importantly, their tax profile and liquidity—is the foundation for your personal financial journey.

For personal finance, we can think of our personal financials as comprising two statements:

Personal income statement / household budget: Income - Expenses (including Taxes) = Savings

Personal balance sheet / net worth statement: Assets - Liabilities (including Taxes) = Net Worth

I’m highlighting taxes in these equations because we have incentives embedded in the U.S. tax code that can influence the way we save and invest. It’s also why it can be powerful to integrate current and future tax liabilities in our financial planning to have a true accounting of net worth.

U.S. retirees have access to government-run programs and government-incentivized programs

Generally, the U.S. government wants you to save over the course of your working life and to invest to support your own retirement. It does so through two methods: a stick and a carrot.

Payroll taxes are the stick

The government forces savings through payroll taxes that support programs it administers for retirees like Social Security (pension/lifetime income) and Medicare (health care).

These are called entitlement programs because the laws that created them require you to be paid the benefits for which you qualify. They are considered mandatory government spending.

Be warned, Congress can at any time adjust the benefits for which you qualify—which they may need to do to control their ballooning costs. In 2023, the major entitlement programs made up about 50% of the U.S. budget.

Tax expenditures are the carrot

The government incentivizes certain types of investments through subsidies to certain tax filers—tax expenditures—which also benefit the private industries that facilitate these investments.

Tax expenditures are revenue losses. Just like other spending and regulatory programs they are discretionary spending—with a twist. They do not have to go through the appropriations process and, if permanent, do not need to be reauthorized by Congress.

For this reason, lawmakers love “hiding” spending in the tax code. These are the Top 30 tax expenditures by revenue losses: Tax Expenditures and the Budget, Explained.

Why am I spending time on U.S. tax policy as an opening to a net worth discussion?

Because the current administration and Congress are negotiating the replacement for the Tax Cuts and Jobs Act of 2017, which is due to expire at the end of this year.

Even if you are many years away from retirement, you have skin in the game. Keep your eyes open for policy changes:

How do they talk about tax expenditures versus spending programs versus regulatory programs—which are all discretionary spending?

Will they adjust qualifications for benefits for any entitlements, the mandatory spending programs?

Who would be the winners and losers of any proposed changes?

We are incentivized to invest in long-term, illiquid assets

Current tax policies incentivize us to build wealth in assets that are relatively long-term and illiquid. This is because policymakers want you to have the funds to support yourself in retirement—and, ideally, pass along wealth to the next generation. They don’t want you to become a burden on the state.

Take advantage of any programs available to you—and track the tax benefits. Yet also stay aware of the overall liquidity profile of your net worth.

Retirement accounts

When deciding how to invest, consider retirement accounts. Compared to investing in a taxable brokerage account, retirement accounts are heavily subsidized.

Unlike brokerage accounts, though, retirement accounts can’t be converted easily to cash without loss of value. If you need to withdraw from them before reaching age 59½, you may face taxes and a 10% early withdrawal penalty.

Pre-tax traditional

When investing in a traditional 401(k), IRA, or like accounts, you can deduct your contribution from gross income in the year that it is made, lowering the amount of income on which you are taxed. You also benefit from having your investments compound tax-free, paying taxes on contributions and investment gains only when you make withdrawals.

After-tax Roth

When using the newer Roth 401(k), IRA, or like accounts, contributions are made after-tax. You don’t get a tax benefit in the year the contribution is made, but your contributions and investment gains compound tax-free and are also tax-free when withdrawn.

In your financial planning, consider diversifying across pre-tax and after-tax retirement accounts to get some benefit in the current tax year while lowering tax liabilities in retirement.

Home ownership

Real estate is another type of illiquid, tax-advantaged investment.

The U.S. government incentivizes home ownership through the mortgage interest deduction and the capital gains exclusion for households who own their primary residence. Also, long-term capital gains are taxed at 0%, 15%, or 20%—much less than earned income—depending on taxable income and filing status.

The mortgage interest deduction only benefits certain tax filers who itemize their deductions, primarily higher income households.

The standard deductions for the 2024 tax year are:

$14,600 – Single or Married Filing Separately

$21,900 – Head of Household

$29,200 – Married Filing Jointly or Qualifying Surviving Spouse

The capital gains exclusions for the 2024 tax year are:

$250,000 — Single

$500,000 — Married Filing Jointly

Because of the preferential treatment of real estate and its lifestyle benefits, many aspire to homeownership.

Yet it is important to note that real estate investing can carry significant financial risks for households. Not only do you need to consider the downpayment and closing costs to acquire a home, but the ongoing costs to carry the home.

Carrying costs may include a fixed mortgage payment—typical in the U.S.—plus variable costs that tend to go up over time like real estate taxes, property insurance, utilities, and maintenance.

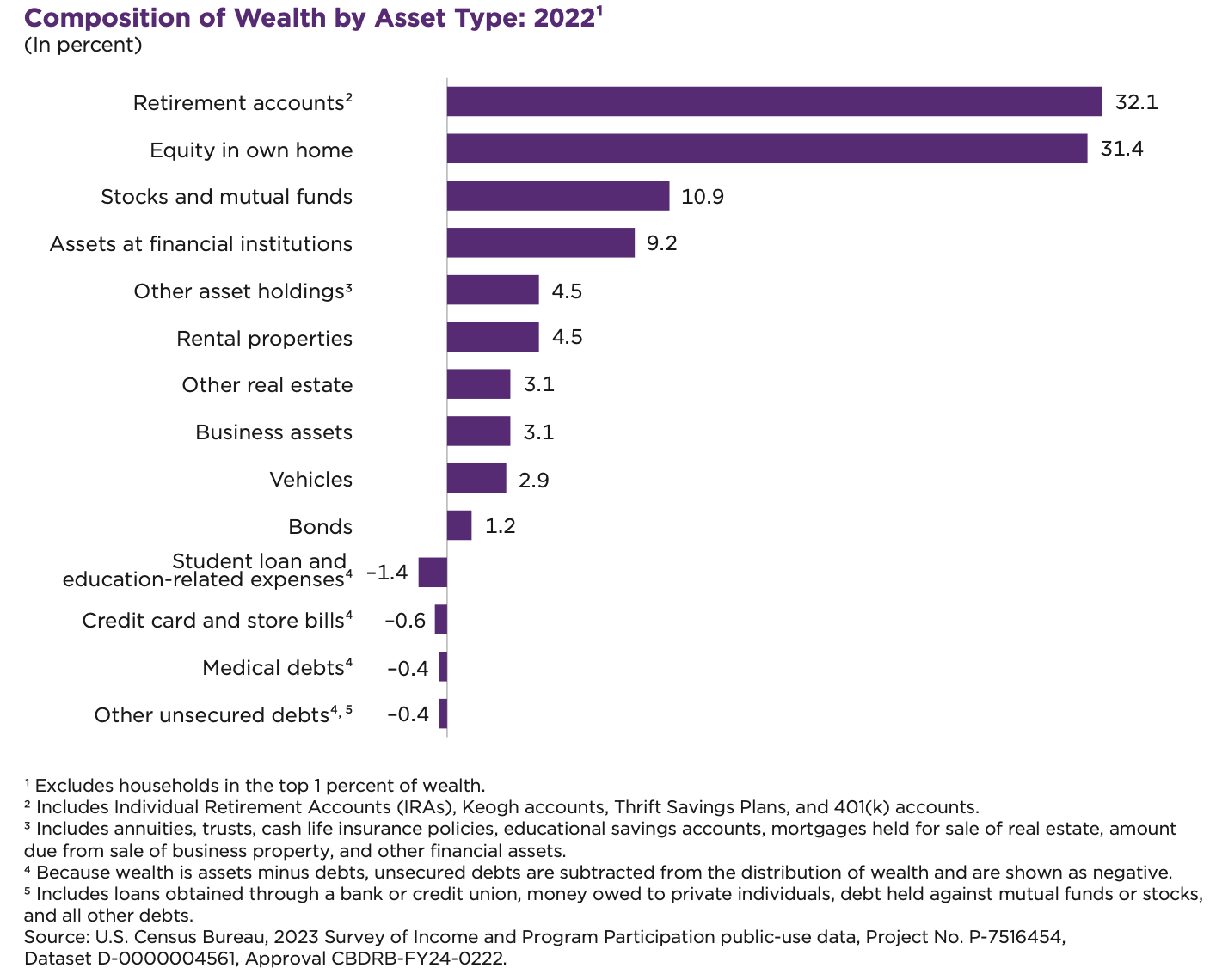

Retirement accounts and home equity comprise over 60% of net worth

Investing through tax-advantaged retirement accounts and buying a home can be powerful ways to build wealth—and it is what most U.S. families do.1

U.S. family finances

If you want to see how your family compares to others and geek out on all things related to U.S. household finances, every three years the Federal Reserve publishes survey data in the Changes in U.S. Family Finances Report; the latest is as of October 2023 with data from 2019-2022.

Considering these years included pre-Covid and post-Covid years and a change in administrations, some interesting stats from this latest report:2

66% of families are homeowners, up slightly.

42% of families have debt secured by their primary residence, unchanged.

54% of families held retirement accounts, up slightly.

20% of families owned a privately held business, an all-time high; nearly half of families in the top income decile own a privately held business.

22% of families carry student debt, increasingly skewed toward high earners.

Real median net worth surged 37%, suggesting a narrowing of the wealth gap.

Measures of financial fragility declined.

Median family net worth was $192,900; top decile was $1,938,000.

Calculating Your Net Worth

As I described above, I believe it is prudent to think of your net worth as comprised of different buckets:

Short-term, liquid versus long-term, illiquid.

Tax-advantaged versus non-tax advantaged, for example:

Taxable account — Brokerage

Tax-deferred account — Traditional 401(k)/IRA

Tax-exempt account — Roth 401(k)/IRA

Triple-tax advantaged account — Health Savings Account (HSA)

Long-term, illiquid and tax-advantaged assets can help you build long-term wealth—and you are subsidized by the government to use them—yet you should consider diversifying to have the means to weather any storm.

To calculate your net worth, add up all your assets and subtract your liabilities. Then ask yourself:

What is the liquidity profile of my net worth?

Do I have liquid emergency funds? How many months of basic expenses will they cover?

What is the tax profile of my net worth?

Am I balancing current and future tax liabilities?

If I have an extra $10,000 in savings, to what would I allocate? Why?

Personal Finance Tools

There are personal finance apps that can help you maintain a household budget and calculate a net worth statement. Top of the Apple Store right now are Nerdwallet, Monarch, Copilot, Rocket Money, and Empower (formerly Personal Capital).

I’ve used Monarch, which is great for budgeting, and Empower, which is better for investments. I warn you, though; these apps can be frustrating.

I want an app to be great at aggregating all my accounts into one view for consolidated reporting. Typically they fail me for three reasons:

The APIs for automatically updating linked accounts are always breaking.

There are many types of assets or certain providers that can’t be linked and need to be entered manually.

If you put business expenses on your personal credit card to be later reimbursed, it can skew your budgeting and cash flow reports.

Additionally, as a single mom I think often about getting hit by the proverbial bus. It’s important to me that I have my net worth documented in such a way the trustee on my daughter’s trust could understand how it is structured and use it to implement my wishes for her.

For my peace of mind, I maintain a detailed spreadsheet that I update quarterly and upload to a DropBox folder containing all my estate planning documents. I share a link to that folder with my trustee and my wealth advisor.

In sum, I think the apps are good visualization tools if you regularly update the linked and manual accounts, and clean transaction data. Though if you want a tool to communicate with your estate executors and professional advisors, in my opinion nothing beats a detailed spreadsheet that you know they can access in the event of an emergency or your premature death.

—Meredith ❤️

Actions Steps:

Keep tabs on the tax policy discussions to understand how they may impact your net worth and investing strategies.

Document your net worth:

Note what is short-term, liquid versus long-term, illiquid

Note what is taxable, tax-deferred, tax-exempt, and triple-tax advantaged

Use the comments to ask me and the community questions.

If you think this would be helpful, forward to others. Referrals are much appreciated!

Resources:

If you want to try Monarch, here is a link for an extended 30-day trial.

(Note: I am not affiliated with Monarch. I am awarded credits toward my annual subscription if you choose to subscribe using this link.)

Disclosure

This newsletter is for informational and recreational purposes only. Any investment products mentioned are for illustration, not recommendations. Always do your own due diligence. Past performance is no guarantee of future results. Meredith Genova is Director of Marketing for AMG National Trust. All opinions expressed are her own and do not reflect the opinion of AMG National Trust or its affiliates.

Sullivan, B., Ghosh, S., & U.S. Census Bureau. (2024). Wealth of Households: 2022. In Current Population Reports (pp. P70BR-202). https://www2.census.gov/library/publications/2024/demo/p70br-202.pdf

Aladangady, A., Bricker, J., Chang, A. C., Goodman, S., Krimmel, J., Moore, K. B., Reber, S., Volz, A. H., Windle, R. A., & Board of Governors of the Federal Reserve System. (2023). Changes in U.S. Family Finances from 2019 to 2022. https://www.federalreserve.gov/publications/files/scf23.pdf